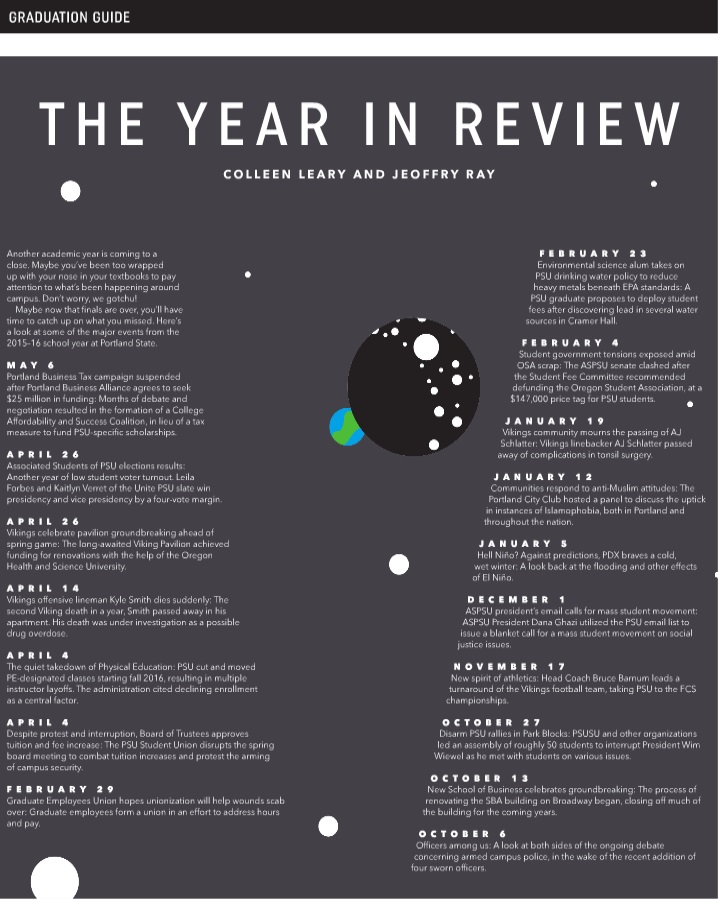

You’re graduating! Congratulations. Well done. Bravo. Good on ya.

If you borrowed money for college through a federal student loan, you are required to begin repayment of the loan 90 days after graduation.

Welcome to the world. A rude welcome, indeed, but rest assured that you are not alone in this predicament and that tools are available to help make the burden manageable.

The good news: It’s likely there is great flexibility in your loan repayment plan options.

The bad news: There is no escape from student loan repayment. It’s crucial to make a plan for paying back the loan; sooner or later, the loan catches up with you and it’s better to examine your options ahead of time.

Here are the nuts and bolts of what to expect regarding your federal student loan:

1) There’s a grace period after graduation before you start paying on the loan.

If you have a federal subsidized or unsubsidized loan, your repayment begins six months after you have graduated, left school, or dropped below half-time in credits, according to studentloans.gov. Perkins loan repayments begin nine months after separating from college. If you have a PLUS loan, repayment begins after final disbursement of funds, although extensions are not uncommon.

Other deferments or extensions can be afforded due to circumstances such as unemployment or a return to college coursework. If any of these options is ever utilized, be sure to find out how interest is handled throughout your deferment period. Interest accumulating during in-school payment deferments adds up quickly.

2) Your loan servicer is an important contact.

As your grace period nears closing, you’ll be contacted by your loan servicer. The loan servicer is an organization that manages loan accounts and collects your payments on behalf of whomever loaned you the money. You will most definitely want to save the loan servicer in your contacts.

Keep their phone, email and any personal contact info if possible. Whatever questions come up regarding your loan in the future will be brought to the loan servicer, and it will save you big hassles to have their information at hand when you need it.

3) You have options regarding your loan repayment plan.

The loan servicer can work with you to iron out the best plan of repayment: a fixed monthly payment that pays off in 10 years (120 payments), a graduated payment that starts low and increases every two years, length of terms to manage the weight of the payment and several other variables.

Many moveable pieces allow flexibility in your repayment planning. Payments can be adjusted based on income, and some borrowers might find themselves eligible for an extended payment plan for a longer period to pay off the loan. This is when it’s important to have retained your loan servicer’s contact info for ease of loan information access. There is no escape from student loan repayment.

4) Consolidating loans is a good idea.

FederalStudentAid.gov recommends consolidating any individual student loans for two reasons: You’ll only have to make one payment each month as opposed to two or three with separate due dates, and you’ll also likely have a lower monthly payment than if the loans are individual. The website also recommends choosing the terms with the fastest payoff you can afford each month. A faster payoff generally means a lower expense to you in the long run.

5) Some professions offer loan forgiveness/assistance.

Professions do exist that allow student loan forgiveness. Conditions always apply and most commit the participating borrower to strict, legally binding contracts. Borrowers working in professions in public service—federal government and certain not-for-profit organizations—may be eligible for loan forgiveness, according to studentaid.ed.gov. Special loan forgiveness incentives are provided for doctors, lawyers, nurses and some teachers. For a completed term of service, some volunteer organizations offer loan forgiveness, such as AmeriCorps, Peace Corps, and Volunteers in Service to America.

6) Get informed. Plan ahead.

Studentaid.gov is a solid resource for estimating future student loan payments and answering other questions you might have specific to your situation. Another great resource is Heather Mattioli at the Portland State Office of Student Financial Aid and Scholarships.

There may be no escape, but with a little effort you can make things easier on yourself.